Operating legally in the UK and avoiding tax issues starts with a clear understanding of the VAT registration threshold. In 2026, this figure remains a key reference point for UK businesses, overseas entrepreneurs, and e-commerce sellers entering or expanding in the British market.

VAT rules are not just about compliance. They directly affect pricing, cash flow, and how your business is perceived by customers, partners, and HMRC. Failing to monitor the threshold properly can lead to penalties, backdated tax bills, and unnecessary administrative stress.

In this guide, we explain how the UK VAT registration threshold works in 2026, when registration becomes mandatory, when voluntary registration makes sense, and how both UK and overseas businesses can stay compliant.

What Is the UK VAT Registration Threshold?

The UK VAT registration threshold is the turnover level at which a business must register for Value Added Tax. Once your taxable turnover exceeds this limit, VAT registration is no longer optional — it becomes a legal requirement.

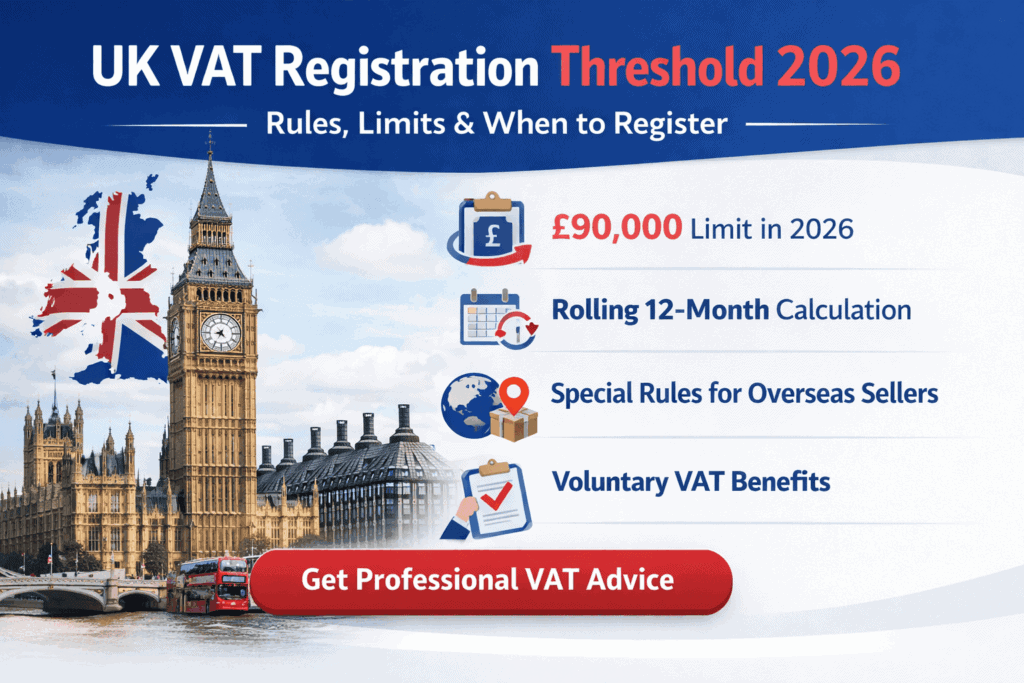

UK VAT Threshold in 2026

As of early 2026, the VAT registration threshold remains £90,000 of taxable turnover. Any business trading in the UK must monitor its turnover closely to avoid crossing this limit unexpectedly.

Once registered, the business must:

- Charge VAT on applicable goods and services

- Submit VAT returns to HMRC

- Comply with Making Tax Digital (MTD) requirements

Many businesses try to stay below the threshold for as long as possible, but once it is reached, delaying registration can be costly.

How the VAT Threshold Is Measured

One of the most common sources of confusion is how the threshold is calculated. The VAT limit does not follow the tax year or calendar year.

Rolling 12-Month Calculation

HMRC uses a rolling 12-month period. This means:

- You must check your turnover at the end of every month

- You look back at the previous 12 months, not forward

- Crossing £90,000 at any point triggers registration

If your turnover exceeds £90,000 over the previous 12 months, you have 30 days to notify HMRC.

Why Monitoring Matters

Regular monitoring is essential. Businesses often breach the threshold unintentionally due to:

- Seasonal sales spikes

- Large one-off contracts

- Growth through online marketplaces

HMRC operates a points-based penalty system, and late registration is frequently detected automatically through digital reporting and bank data.

What Counts Toward the £90,000 VAT Threshold?

VAT registration is based on taxable turnover, not profit.

Included in Taxable Turnover

You must include:

- Standard-rated sales (20%) – most goods and services

- Reduced-rated sales (5%) – such as domestic energy

- Zero-rated sales (0%) – including most food, books, and children’s clothing

Excluded from the Calculation

You should exclude:

- VAT-exempt income – insurance, healthcare, postage stamps

- Out-of-scope income – grants, statutory payments, non-business income

Common Mistake: Zero-Rated Sales

A frequent error is assuming that zero-rated sales do not count toward the threshold. They do. Although VAT is charged at 0%, these sales are still taxable and must be included. This misunderstanding is one of the most common reasons businesses are forced into late VAT registration.

When VAT Registration Is Mandatory in 2026

VAT registration becomes compulsory if either of the following applies:

Mandatory Registration Triggers

- Your taxable turnover exceeded £90,000 during the previous 12 months

- You expect your turnover to exceed £90,000 within the next 30 days (for example, after securing a major contract)

Once triggered, you have 30 days to apply. HMRC will confirm the effective registration date, from which VAT must be charged.

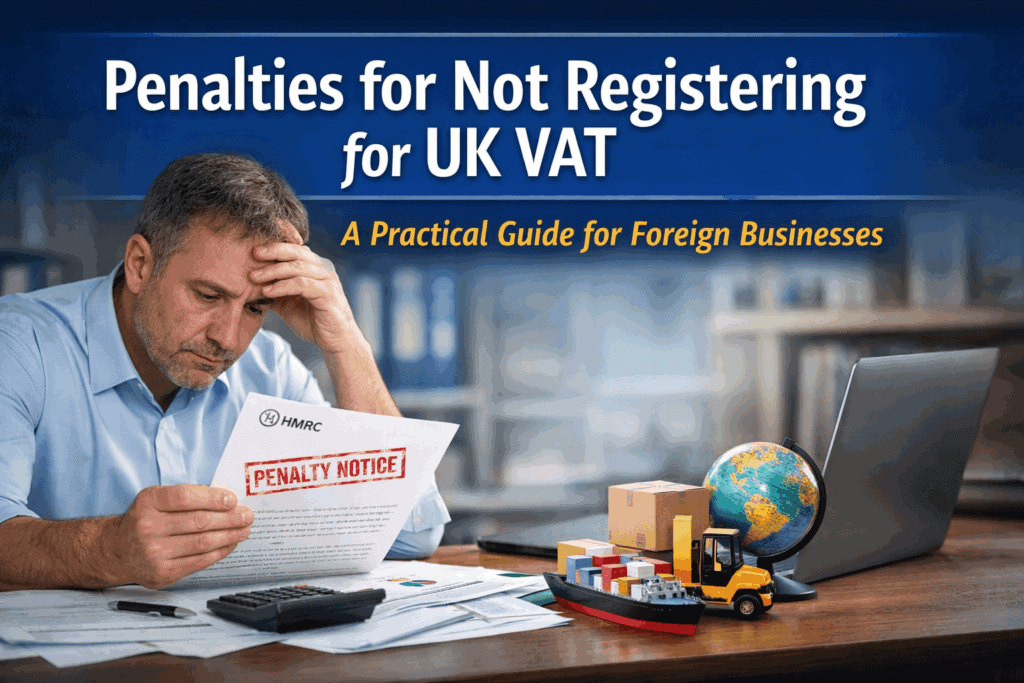

Consequences of Late Registration

Missing the deadline can result in:

- Financial penalties

- Backdated VAT liabilities

- Interest on unpaid VAT

In 2026, HMRC uses enhanced data-matching, marketplace reporting, and banking information to identify late registrations quickly.

Voluntary VAT Registration: Is It Worth It?

Even if your turnover is below £90,000, voluntary VAT registration can be a sensible strategic decision for some businesses.

Benefits of Voluntary Registration

- Reclaiming input VAT on equipment, software, and professional services

- Improved credibility with UK clients and corporate partners

- Marketplace access, as some platforms require VAT registration

- Smoother growth, avoiding a rushed registration later

Who Often Registers Voluntarily?

- E-commerce sellers using Amazon or eBay

- Consultants working mainly with VAT-registered clients

- SaaS and tech startups with high upfront costs

- B2B businesses where clients can reclaim VAT

Voluntary registration does increase reporting obligations, so professional advice is recommended to ensure the benefits outweigh the added administration.

Overseas Businesses and UK VAT Rules in 2026

Special VAT rules apply to Non-Established Taxable Persons (NETPs) — businesses based outside the UK.

No VAT Threshold for Overseas Sellers

For most overseas businesses, the £90,000 threshold does not apply. Instead, VAT registration may be required from the first taxable sale.

You May Need to Register If You:

- Store goods in UK warehouses

- Use UK fulfilment centres, including Amazon FBA

- Sell directly to UK customers

- Operate via online marketplaces

- Supply digital or cross-border services to UK consumers

This “nil threshold” means there is no turnover buffer. Even a small first sale can trigger VAT obligations.

HMRC’s focus on overseas sellers has intensified, supported by data sharing with online platforms. Professional VAT support is often essential to avoid errors and retrospective tax bills.

Common VAT Registration Mistakes in 2026

Even experienced business owners make mistakes during VAT registration.

Frequent Errors to Avoid

- Miscalculating taxable turnover

- Registering too late

- Selecting the wrong VAT scheme

- Submitting inconsistent or incomplete information

- Misunderstanding post-registration obligations

Any of these can delay your VAT number, disrupt invoicing, and prevent VAT reclaims.

Why Use a Professional UK VAT Registration Service?

VAT registration involves more than completing an online form. It requires a clear understanding of your business model, transactions, and future growth plans.

Key Advantages of Professional Support

- Tailored assessment of your VAT obligations

- Accurate handling of HMRC requirements

- Correct timing and documentation

- Strategic VAT planning from day one

Professional assistance reduces delays, prevents costly mistakes, and protects your cash flow.

UK VAT Registration with vatnumberuk.com

At vatnumberuk.com, we specialise in UK VAT registration for both UK-based businesses and international companies.

How We Help

- Eligibility assessment, including overseas and nil-threshold cases

- Full application management via HMRC systems

- Multilingual support in English and Russian

- E-commerce and marketplace expertise

- Risk reduction, minimising HMRC queries and delays

We monitor regulatory changes closely to ensure your VAT registration is handled correctly and efficiently in 2026.

Final Thoughts on the UK VAT Registration Threshold 2026

Key Points to Remember

- The VAT threshold in 2026 is £90,000

- It is based on a rolling 12-month calculation

- Zero-rated sales count toward the limit

- Overseas businesses often face a nil threshold

- Late registration can lead to penalties and backdated VAT

Professional guidance ensures compliance, saves time, and reduces financial risk.

Frequently Asked Questions: UK VAT Registration Threshold 2026

What is the UK VAT registration threshold in 2026?

The threshold remains £90,000. If your taxable turnover exceeds this amount within any rolling 12-month period, VAT registration is mandatory.

Is the VAT threshold based on a calendar year?

No. It is calculated on a rolling 12-month basis and must be reviewed monthly.

Can I register for VAT voluntarily?

Yes. Many businesses choose voluntary registration to reclaim VAT, improve credibility, or meet marketplace requirements.

Do zero-rated sales count toward the threshold?

Yes. Zero-rated sales are taxable and must be included when calculating turnover.

Does the VAT threshold apply to overseas businesses?

Usually not. Overseas sellers often need to register from their first taxable sale.

How long does VAT registration take in 2026?

Most applications take 2–6 weeks, though complex cases can take longer.

What happens if I register late?

You may face penalties, backdated VAT liabilities, and interest charges.

{kind=link}

{kind=link}

{kind=link}